ArcelorMittal partners AWS to automate global operations Midrex to build new DRI plant for US Steel Flair Writing wins ₹200 million fresh orders Green steel projects face major global delays

Global crude steel production in August 2025 was broadly flat year-on-year, slipping slightly month-on-month as mills trimmed output amid weak margins and soft demand.

China: Marginal decline as policymakers balanced output control with domestic demand support.

India: Solid growth driven by infrastructure and robust mill utilizations.

U.S. & Turkey: Mild gains on improved domestic orders and stable pricing.

Japan, South Korea & Russia: Contractions on weaker exports and maintenance outages.

EU Core (e.g., Germany): Continued softness reflecting subdued industrial activity.

Cumulative global production for the first eight months of 2025 remained slightly below last year, with Asia cushioning declines from Europe and parts of the CIS.

Construction and manufacturing demand stayed uneven across regions. Export orders were mixed, and spreads were pressured by raw-material volatility and cautious buying.

China’s policy signals on output controls vs. stimulus.

India’s run-rate into the festive/build season.

EU industrial recovery and gas/power cost trajectory.

Export competitiveness as currencies and freight shift.

Outlook

Near term, global output is likely to track sideways, with upside tied to steadier construction activity in Asia and any incremental stimulus in major economies. Risks include weaker export demand, cost inflation in coking coal/energy, and persistent EU industrial softness.

Also Read : Global Stainless Steel Market Shows Resilient Growth in Q2 2025 International intrigue in Vietnam's rare earth

US–UK Trade Deal Slashes Car and Aerospace Tariffs, Steel Talks Ongoing The United States and...

USA 17-Jun-2025

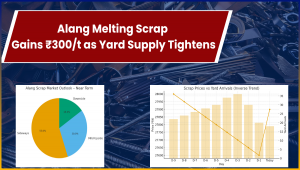

Alang Melting Scrap Up ₹300/t DoD Snapshot Melting scrap prices at Alang (ship-breaking yard, Guja...

Renewables 17-Nov-2025

According to analysts at BofA Securities, the metals and mining sector in India, particularly steel...

Raw Material 20-Jan-2024

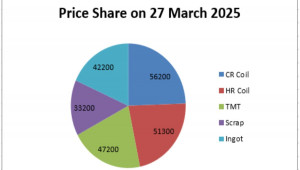

Global Market Signals + 🇮🇳 Indian Price Trends = Key ForecastsAs we close out March 2025, both domes...

Business 27-Mar-2025

Steel is one of the most recycled materials in the world. Every time a building is demolished or a c...

Business 02-May-2025

India and France have developed strategic ties for over 25 years since 1998, marked by significant b...

Business 25-Jan-2024