ArcelorMittal partners AWS to automate global operations Midrex to build new DRI plant for US Steel Flair Writing wins ₹200 million fresh orders Green steel projects face major global delays

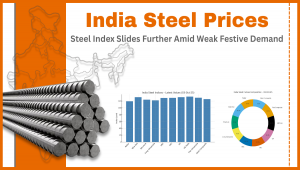

BigMint’s India Steel Composite Index recorded another weekly drop of 0.5% as of October 24, 2025, reflecting continued market weakness through the Diwali holiday period. Trading activity remained muted, while steel prices stayed near a five-year low due to high inventories and subdued construction demand.

Flat product prices continued to soften amid limited restocking. Hot Rolled Coil (HRC) declined by ₹300 per tonne to around ₹48,000/t, while Cold Rolled Coil (CRC) dropped ₹200/t to ₹55,500/t. Mills had already reduced list prices earlier in the month by ₹750–1,500/t to stimulate sales, but buying momentum remained sluggish.

Blast Furnace (BF) Rebar slipped ₹100/t week-on-week to ₹46,800/t ex-Mumbai, while Induction Furnace (IF) Rebar stayed largely stable across regional markets due to lower activity during the festive break.

Although India’s overall steel consumption has grown around 8% year-on-year, oversupply and global demand uncertainty continue to weigh on domestic prices. Analysts expect a modest rebound post-Diwali as infrastructure and construction activity resume, but price recovery may stay capped by persistent global overcapacity.

Also Read : SteelBazaar Insight: Global Coal Production Trends Signal Shift in Energy Strategy Rebars Lead the Charge: Decoding the 2024 Steel Long Products Market

Snapshot India’s steel market continued to face pressure in early October 2025, with BigMin...

India 06-Oct-2025

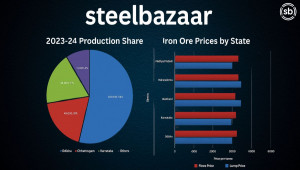

India’s iron ore production for FY 2023–24 stands at 262 million tonnes, with Odisha alo...

Business 21-Apr-2025

Vietnam is expanding its extraction of rare earth minerals, which are crucial for modern technology...

China 27-Jan-2024

Steel majors expect the budget to boost economic growth and benefit people by supporting critical in...

Business 02-Feb-2024

India's pursuit of a cleaner and more diverse energy landscape takes a significant leap forward with...

Oil & Gas 08-Feb-2024

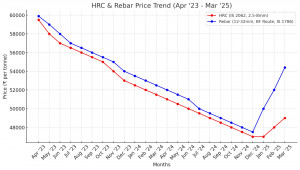

Steel industry analysts report a significant decline in Hot Rolled Coil (HRC) and Rebar prices over...

Business 20-Mar-2025