ArcelorMittal partners AWS to automate global operations Midrex to build new DRI plant for US Steel Flair Writing wins ₹200 million fresh orders Green steel projects face major global delays

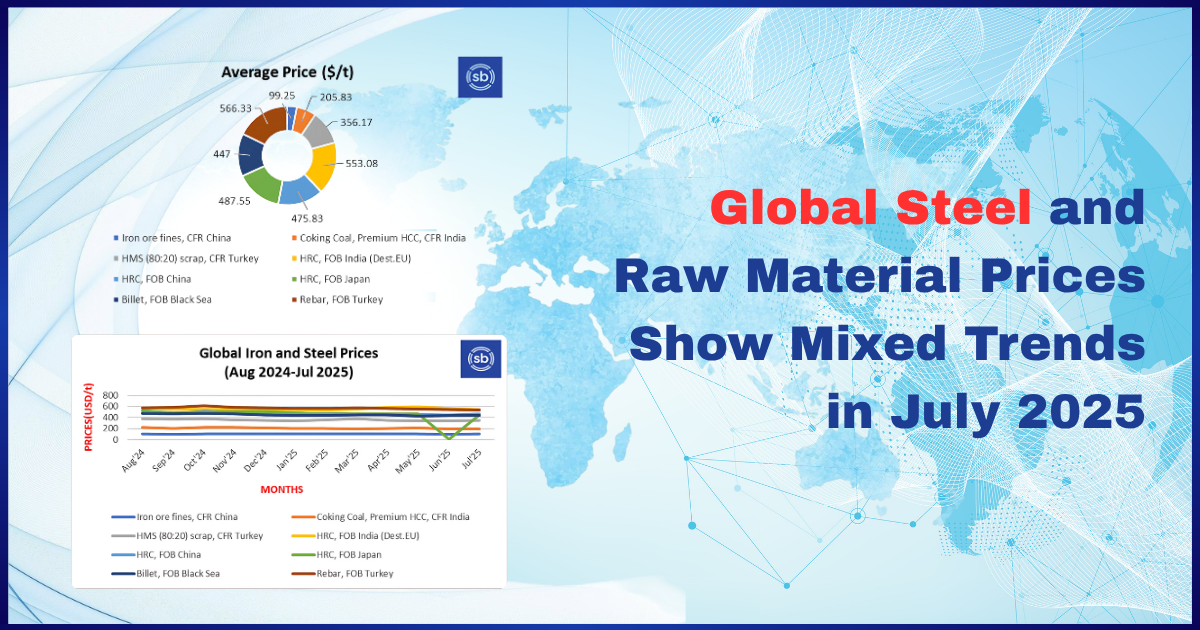

The global steel and raw materials market saw uneven pricing trends in July 2025, reflecting shifting demand and economic uncertainties. While some segments gained modest ground, overall momentum remained weak.

Iron ore prices showed a slight recovery, driven by improved buying activity in China and favorable sentiment in futures markets. However, average prices stayed below $100 per tonne, indicating fragile market confidence.

Hot-rolled coil (HRC) export offers from China increased by around $19 per tonne compared to June. This rise was supported by higher domestic futures and expectations of policy changes to boost industrial demand.

Turkey’s deep-sea scrap prices also strengthened, buoyed by consistent demand from construction and improved purchasing activity. In contrast, Indian HRC export prices to the EU dropped sharply to approximately $541 per tonne FOB, pressured by weak European demand and rising global competition.

Despite these mixed results, market sentiment is cautiously optimistic heading into August. Industry players are watching for signs of stabilization, with hopes pinned on policy support and seasonal demand recovery to drive a more consistent rebound.

Also Read : International intrigue in Vietnam's rare earth Global Steel Output: Flat Overall, Diverging by Region (Aug 2025)

Snapshot TMT bar prices were broadly unchanged this week as mills and stockists navigated soft site...

Construction 30-Oct-2025

Prices of SteelFollowing a trend of softening in early 2025, prices bo...

Business 06-Jun-2025

According to analysts at BofA Securities, the metals and mining sector in India, particularly steel...

Raw Material 20-Jan-2024

In a bid to showcase India's burgeoning economic potential and foster global partnerships, the gover...

Business 14-Feb-2024

Gujarat is gearing up to host a game-changing marvel, the world's largest steel plant, declared by t...

Large Corporate 23-Jan-2024

India: Weak Festive Demand Indian mills are buying cautiously amid the festive-season slowdown. S...

Asia 30-Sep-2025