ArcelorMittal partners AWS to automate global operations Midrex to build new DRI plant for US Steel Flair Writing wins ₹200 million fresh orders Green steel projects face major global delays

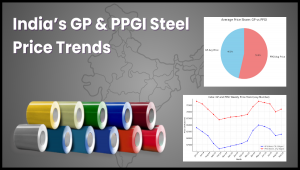

India’s steel market continued to face pressure in early October 2025, with BigMint’s India Steel Composite Index touching a near five-year low. The decline was driven by weak construction demand, persistent monsoon rains, and a sluggish festive season that limited restocking activity.

Hot Rolled Coil (HRC): Prices slipped by ₹600 per tonne week-on-week to around ₹48,500/t.

Cold Rolled Coil (CRC): Marginal dip to ₹55,900/t, reflecting lower automotive and appliance sector demand.

Rising imports during September added to the pressure on domestic mills, capping any recovery attempts.

Blast Furnace (BF) Rebar: Gained ₹400/t to ₹47,200/t on selective restocking.

Induction Furnace (IF) Rebar: Remained muted, with rainfall and holidays slowing site activity and keeping inventories elevated.

The near-term outlook remains cautious as participants await post-festive policy cues and infrastructure project restarts. A clearer revival in pricing is expected only if construction activity improves and domestic offtake strengthens toward year-end.

Also Read : BALCO Produces First Metal from India’s Largest Aluminium Smelter Decoding the Future of Global Steel Demand: India to Lead Consumption

Marking a pivotal development, the government has launched an initiative mandating steel producers t...

Ferrous 10-Jan-2024

Demand Weakness and Inventory Overhang India’s coated steel market is witnessing subdued de...

India 12-Sep-2025

Decoding the Future of Global Steel Demand: India to Lead Consumption Global Steel Demand at a Cros...

India 19-Aug-2025

India's engineering goods exports experienced a 8.62% year-on-year decline in February 2025, droppin...

Business 25-Mar-2025

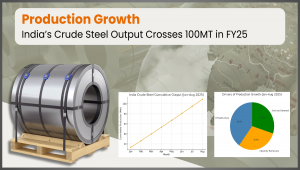

India’s crude steel production surpassed 100 million tonnes in Jan–Aug 2025, signalling...

India 15-Sep-2025

Vietnam is expanding its extraction of rare earth minerals, which are crucial for modern technology...

China 27-Jan-2024