Gadchiroli pitched as Maharashtra’s future green steel hub India set to drive next global steel demand wave Italy crude steel output rises 3.1% in May Green steel progress remains slow worldwide

China's imports of unwrought aluminium more than doubled year on year in 2023, hitting the second-largest annual total since the turn of the century. It has raised eyebrows in the global market, with Russian metal accounting for 76% of the total. This increase underscores Russia's growing sway over China's aluminium market dynamics and is a substantial departure from the composition of inbound shipments in 2021.

China's primary metal imports increased to 1.54 million metric tonnes (MMT) from 668,000 tonnes in 2022 but fell short of the record 1.58 MMT set in 2021. The composition of inbound shipments significantly differed between the 2021 and 2023 peaks.

The Symbiotic Relationship: Russia and China in the Aluminium Market:

As penal import taxes and sanctions altered global trade patterns, Russia and China increasingly relied on each other in the aluminium market. The disruption in Russian trade patterns resulted in mutual reliance, with China emerging as a critical market for Russian aluminium and Russia becoming the key supplier to China's expanding demand.

Russian metal accounted for only 18% of 2021 quantities, up from 76% last year after penal import taxes in the United States and self-sanctioning in areas of Europe upset previous Russian trading patterns. In the aluminium market, China and Russia depend on one another more.

Can China, the largest producer of aluminium in the world, continue to absorb what others find objectionable?

Additionally, Russia has been shipping China additional unwrought aluminium alloys. Russian material imports increased by 11% to 63,000 tonnes last year, while overall Chinese alloy imports decreased by 11% from 2022. The total from 2021 and last year was almost twice as much.

Chinese alumina, the intermediate product in the industrial cycle between bauxite and refined metal, has been used to process some of the metal transported from Russia to China.

From Indian to Russian Aluminium; Rusal's Strategic Moves

Indian-brand aluminium accounted for the lion's share of 2021's bumper imports. More than half of all inbound shipments were made up of 855,000 tonnes.

On the other hand, Chinese imports of Russian-brand aluminium totalled only 291,000 tonnes in the last full year of the trade before the February 2022 invasion of Ukraine. Russian material imports reached 462,000 tonnes in 2022 before skyrocketing to 1.18 million tonnes in the previous year. During the same period, imports of Indian metal decreased to just 98,000 tonnes.

The Russian aluminium behemoth, Rusal lost access to its Ukrainian refinery and its joint venture Australian factory shortly after Vladimir Putin's "special military operation" began. The corporation has been increasingly dependent on Chinese suppliers; in October of last year, it acquired a 30% share in Hebei Wenfeng New Materials, the company that runs a newly constructed alumina refinery with an annual capacity of 4.8 million tonnes.

In the same way as Rusal Metal controls most of China's imports of raw aluminium, the business also contributes significantly to China's alumina exports. Shipments to Russia were 1.12 million tonnes last year, accounting for 88% of overall export volumes. In 2021, the two nations' combined alumina commerce amounted to a meagre 1,747 tonnes. Indeed, given recent stress signals in China's production sector, it is improbable that China would export much alumina without the Russian connection.

Sino-Russian Trade: China Absorbing Russian Metal

China, as the market of last resort, received Russian metal that would have otherwise flooded Western warehouses. High inventories of Russian content are a problem for LME, which has led to discussions about suspending Russian brands or changing delivery policies to comply with arbitrary government sanctions.

By the end of December, 338,375 tonnes of Russian aluminium, or 90% of the total registered inventory, were on the LME warrant. The high ratio has reignited the long-simmering debate over whether the exchange should prohibit Russian brands instead of changing its delivery policies to permit unilateral government restrictions like the US import levies. Obviously, if China did not receive about 25% of Rusal's production, the LME's predicament would be far worse.

Is Sino-Russia commerce the new normal? As long as China can continue to take in such substantial amounts of primary metal, it appears likely. China's role as the world's top aluminium producer in absorbing considerable primary metal inflows becomes critical.

China produced 59% of the world's aluminium last year, but the country's output growth has slowed from double digits in the 2000s to just 3% last year and 4% in 2021 and 2022.

China's consumption is still high despite a slowdown in output growth, thanks to the country's energy transition industries and solid new-energy technology exports.

Geopolitical Implications in China's Aluminium Market:

China's position as the world's largest aluminium producer is threatened as the country's output growth slows and its yearly production capacity gets closer to the 45 million tonnes government cap. This indicates that not many new smelters are being constructed and that run rates in regions affected by drought, like Yunnan, are frequently hampered by a lack of hydropower.

In the meantime, demand from industries undergoing energy transition appears to remain strong partly because of solid exports of new energy technologies like solar panels. There is no indication of a significant excess in the mainland market. The amount of stocks listed on the Shanghai Futures Exchange is 101,537 tonnes.

Semi-fabricated product exports, which have historically been a reliable indicator of a domestic market oversupply, decreased by 12% in 2022 compared to 2023. Of course, some of the items "imported" in 2017 are likely being held in a Chinese bonded warehouse.

Official customs data make no distinction between metal imported for consumption in China and metal stored for long periods to be used as collateral. Either way, it is positive news for the LME and the Western market.

The geopolitical landscape complicates the aluminium trade, with trading Russian metal growing more difficult as Western policymakers tighten sanctions. British nationals are no longer permitted to deal in Russian metal in person, which has caused major problems for a London-based exchange.

There are now rising proposals for the European Union to increase economic pressure on Russia by expanding sanctions on Russian aluminium from specialised goods to primary metal. Russian aluminium, which has escaped a complete prohibition due to sanctions, appears to become increasingly harder to sell to Western consumers. It is not just Rusal will be hoping Chinese consumers continue to be interested in buying aluminium imports.

Also Read : Base Metals Outlook 2024: A Comprehensive Analysis Revamping Energy: India’s Call for Domestic Coal Adoption

India is actively coordinating its steel sector with sustainable practices as the globe moves toward...

Ferrous 30-Jan-2024

South India stands at the threshold of a transformational steel boom—...

Business 02-Jun-2025

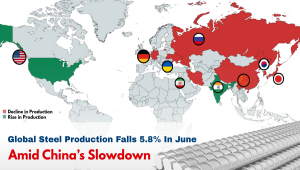

Global Steel Production Drops 5.8% in June, Led by China’s Slowdown Global crude steel output...

Press Releases 24-Jul-2025

In recent weeks, Qatar Energy and Indian companies have been on the verge of finalising a groundbrea...

Renewables 22-Jan-2024

Market Snapshot India’s steel market has entered a correction phase, with domestic prices sli...

India 24-Oct-2025

According to analysts at BofA Securities, the metals and mining sector in India, particularly steel...

Raw Material 20-Jan-2024