Gadchiroli pitched as Maharashtra’s future green steel hub India set to drive next global steel demand wave Italy crude steel output rises 3.1% in May Green steel progress remains slow worldwide

The base metals industry had challenges in 2023, with numerous factors leading to a less-than-ideal result. Except for copper, which held steady, most other base metals went through a difficult time due to China's economic problems, a pessimistic outlook for global growth, rising interest rates, and concerns about oversupply.

Recap of 2023 Performance

Copper rose 2% last year, while aluminium and lead prices fell 1% and 4%, respectively. Meanwhile, zinc was the worst-performing metal in the group, falling more than 14% in the domestic market and 10% across the globe.

The price drop was primarily caused by decreasing economic activity in major economies, which reduced demand for some base metals despite an increasing supply.

China is the world's largest user of base metals, accounting for around 50% of the global production. The country's industrial sector saw contractions in seven of the last eight months of 2023. The property sector crisis and rising inflationary economic threats resulted in lacklustre demand for industrial goods over the preceding year.

Global Economic Challenges

The global economy is currently confronting structural macroeconomic issues. The two-year Russian-Ukraine conflict, Hamas' attack on Israel, and Israel's military response all pose substantial difficulties to the global economy and consumption in 2023.

The manufacturing sectors in the United States and Europe were also steadily contracting. The factory activity in Europe fell to levels not seen in eighteen months, and further data points to a recession across the EU. Similarly, rising interest rates caused the US manufacturing sector to contract drastically.

Growing interest rates made borrowing more expensive, discouraging company investment and consumer spending, which slowed global growth. The US Federal Open Market Committee (FOMC) increased interest rates four times in 2023, driving up borrowing prices.

Outlook for 2024

According to predictions, the markets will probably be evenly balanced in 2024, which means the outlook for metal prices will remain neutral. The main threats to the price prediction are reduced demand from China and other wealthy countries and increased geopolitical tensions.

Meanwhile, China's stimulus efforts, industrial revival in key consuming nations, and a rate drop by the US Federal Reserve are all positive macroeconomic factors that could influence metal prices in 2024. Government expenditure initiatives in the US, Europe, and China can also help with the metal-dependent infrastructure development and energy shift.

This year will probably see significant growth in the green demand sector, even though the overall industrial demand is only expected to stagnate. Countries like China and India are accelerating the renewable energy sector by increasing the capacity of solar and wind power generation to achieve climate commitments. This could be the increasingly crucial new cycle booster for the base metal complex.

Other base metals are expected to be oversupplied this year, except copper. Following high-profile mine delays and suspensions in 2023, copper has the tightest fundamental outlook, with a refined market supply-demand imbalance this year.

Navigating the base metals market in 2024 demands a thorough awareness of the interplay between economic, geopolitical, and supply-side issues. While challenges remain, opportunities in the green demand sector and supportive government measures may provide investors and industry players a bright spot.

Also Read : Russia's Strategic Role: Understanding the Integral Relationship Driving China's Aluminium Import Surge Revamping Energy: India’s Call for Domestic Coal Adoption

Fossil fuels continue to meet more than 80% of the world’s energy needs despite a record growt...

Energy 10-Jan-2024

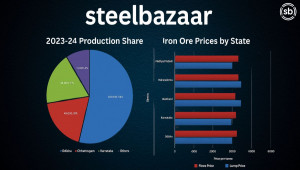

India’s iron ore production for FY 2023–24 stands at 262 million tonnes, with Odisha alo...

Business 21-Apr-2025

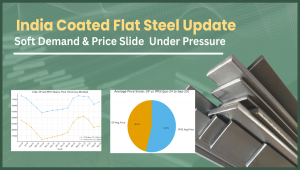

Indian Coated Flat Steel: Soft Demand, Prices Ease on Cautious Buying The coated flat steel market...

India 19-Sep-2025

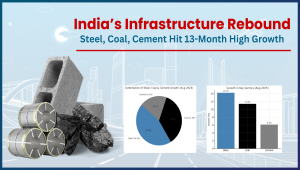

Core Sector Growth Hits 13-Month HighIndia’s eight core sectors recorded 6.3% growth in August...

India 23-Sep-2025

March 2025 brought significant developments in the steel market, shaping domestic and global trade d...

Business 26-Mar-2025

India is set to sign trade facilitation deals with five more key partners over the next three months...

Press Releases 19-Dec-2023