Gadchiroli pitched as Maharashtra’s future green steel hub India set to drive next global steel demand wave Italy crude steel output rises 3.1% in May Green steel progress remains slow worldwide

The Red Sea has long been an essential route for transferring crude oil and refined products between important places in the intricate world of international energy exchange. However, this strategic waterway has been a source of concern in recent months, with rising tensions driven by the ongoing Houthi rebellion. In this context, Indian refiners find themselves at a crossroads, forced to navigate the shifting tides of geopolitical risk while assuring the uninterrupted flow of critical supplies.

With no indication that the Houthi threat in the Red Sea is subsiding, Indian refiners are shifting diesel imports to Asia, with loadings to Europe reaching a low in January 2024.

As Indian and West Asian refiners become more hesitant to transit the Red Sea, which accounts for 8.5 million barrels per day (mb/d) of crude oil and refined product trade, to export diesel to Europe, cargoes from the United States are filling the supply gap, according to Wood Mackenzie (WoodMac) in its most recent report.

Shifting Trade Dynamics: Diesel Redirected to Asia as European Demand Wanes

According to trade sources, diesel loadings from India to Europe reached their lowest level in several years in January 2024. Refiners are looking to Asia since there are now more opportunities for sales due to unscheduled refinery repairs. Domestic refiners sell diesel in Singapore and a few other East Asian nations.

India transported about 3,02,000 barrels per day (b/d) of diesel last month, down from almost 5,51,000 b/d in December 2023, a nearly 45% decrease, according to oil analytics firm Kpler. Shipments to the UK and nine other countries, such as France, the Netherlands, and Spain, decreased from 4,25,193 b/d to 1,52,010 b/d.

The Petroleum Planning and Analysis Cell (PPAC) estimates that diesel exports fell by 29% month on month in January. “European distillate imports become more costly as the Middle East and West Coast India volumes travel further at elevated freight rates,” said the consultancy.

Avoiding Red Sea

More than half of middle distillate flows to Europe were rerouted through the Cape of Good Hope (COGH) in January 2024, while total East-West flows fell substantially as Indian diesel loadings stalled and shifted to Asia, expecting a re-basing of European prices, WoodMac reported.

The consultancy anticipates that the present West Asian conflict will be limited to Israel and Hamas, with no severe spillover into the rest of the area. It also estimates that the war and Red Sea transit problems will last until the end of Q3 2024, with ships continuing to avoid the Red Sea throughout this period.

“Spiking freight rates and insurance premiums have forced Indian diesel loadings to Europe to fall to zero in the last weeks of January as refiners and traders weighed up the risk and longer sail time, opting instead to send barrels East. This will heavily impact arrival volumes into Europe in the next couple of months while also weighing on Asian distillate balances,” WoodMac said.

Freight Rate Surge and Logistics Challenges

The Red Sea accounts for 5.5 mb/d, or 15% of total crude oil commerce, while total refined petroleum product movements average around 3 mb/d, accounting for 15% of global refined product trade, according to WoodMac.

“Despite US and UK strikes on Houthi targets, the interruption in the Bab el-Mandeb strait shows little signs of abating, with over 20% of oil tanker traffic now diverting around the COGH. This adds at least two weeks to trip timings, resulting in increased tonne-mile demand, higher freight prices, and more product cracks”, it added. According to Wood Mackenzie, trade patterns will change, with more US distillates travelling to Europe and Middle Eastern goods travelling to the Americas and Asia.

In a February 1 report, the US EIA said: “Major oil and natural gas companies that are avoiding the Red Sea include Equinor, which operates mostly natural gas carriers, and bp, which operates both oil and natural gas carriers. As of January 23, 2024, other major energy companies pausing Red Sea transits include Euronav, QatarEnergy, Torm, Shell, and Reliance.”

In a report released on February 9, India Ratings & Research (Ind-Ra) stated that the first response is seen in the 150% increase in freight rates over the previous 45 days. The route accounted for 40% of all oil imports and 24% of total exports from April to October 2023.

The Suez Canal handles between 20 and 25% of India’s foreign trade logistics, affecting important goods, including crude oil, automobiles, accessories, chemicals, textiles, iron, and steel.

As the Red Sea situation persists, stakeholders in the energy industry must stay watchful and adaptable in the face of shifting geopolitical forces. With freight costs rising and trade flows moving dramatically, resilience and foresight are essential.

Also Read : Identifying the Impact of Red Sea Crisis on Global Commodity Markets Crude truth: Why India will have to rely on fossil fuels for longer than expected

The steel industry is heating up in 2025 — but not just from furnaces. Global players are adju...

Business 23-May-2025

The Red Sea issue, fueled by attacks on commercial vessels by Iranian-backed Houthis, is changing gl...

Energy 22-Jan-2024

China's imports of unwrought aluminium more than doubled year on year in 2023, hitting the second-la...

Non-Ferrous 31-Jan-2024

India remained a net steel importer in January–October 2025 even as inbound shipments declined...

Construction 20-Nov-2025

A concise Q2 FY25 analysis of Tata Steel, JSW Steel, SAIL, and Jindal Steel’s performanc...

Business 13-May-2025

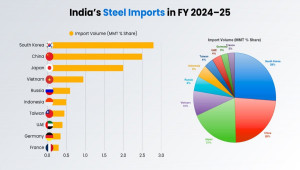

India's steel import volumes witnessed a notable rise in FY 2024–25, reaffirming the nation&rs...

Business 26-May-2025