Gadchiroli pitched as Maharashtra’s future green steel hub India set to drive next global steel demand wave Italy crude steel output rises 3.1% in May Green steel progress remains slow worldwide

SteelBazaar Insight

Steel & Raw Material Price Trends in FY'25: What Drove the Market?

As FY'25 draws to a close, the Indian steel industry has seen a complex mix of opportunities and challenges. Here’s a summary of what influenced the price trends across steel and key raw materials during the year.

🔩 Iron Ore & Pellets:

Domestic iron ore prices dipped by 4% YoY as steel demand weakened and production rose. India's iron ore output climbed to 263 million tonnes (April–Feb FY'25), but exports fell due to reduced demand from China.

Globally, iron ore prices dropped 17% YoY to $100/ton (CNF Rizhao), driven by a glut in inventory at Chinese ports, touching 143 million tonnes.

Pellet prices also declined marginally by 1.5% as sluggish finished steel demand continued.

Coal:

Coking coal prices (CFR India) dropped by 5%, reflecting subdued buying by domestic steelmakers.

In contrast, non-coking coal prices remained stable, supported by robust domestic production which crossed 1 billion tonnes for the first time. Import reliance also eased by 9% YoY.

🔧 Scrap:

Scrap prices weakened across the board due to higher local generation and reduced imports. HMS (80:20) DAP-Mumbai and shredded scrap (CNF Nhava Sheva) both declined by 5%.

India’s domestic scrap generation rose 7% YoY to 32 million tonnes, and imports shrank by 16%, favoring cost-efficient domestic material.

🧱 Sponge Iron:

Prices declined by 7%, pressured by increased output. India's sponge iron capacity surged to 68.8 million tonnes, and production is expected to reach 55 million tonnes in FY'25.

🏗️ Long Steel Products:

Billets: Fell by 4% due to easing prices in scrap and sponge iron.

Rebars (BF/IF grades): Declined 1%–4%, though support came from NHAI’s new vendor verification norms and limited supply due to mill shutdowns.

Wire Rods: Dipped 4% amid lackluster infrastructure demand.

Global Billets (Black Sea): Dropped 6% on lower demand from Turkiye and Egypt.

📉 HRC (Hot Rolled Coils):

India’s domestic HRC prices saw a steep 11% YoY fall to INR 50,030/t, affected by rising imports.

India’s steel imports reached 10 million tonnes, up 8% YoY.

Global prices also fell sharply:

FOB East Coast India: –13%

FOB Tokyo: –15%

FOB Black Sea: –14%

CNF Antwerp: –13%

Chinese exports surpassed 110 million tonnes, disrupting pricing across Asian and Middle Eastern markets.

🔮 SteelBazaar Outlook for FY'26:

With geopolitical risks, possible tariff interventions (like safeguard duties), and sustained global oversupply, prices are expected to remain under pressure or volatile in the near term.

India may consider protectionist measures to support domestic mills and discourage undercutting by foreign suppliers.

📊 SteelBazaar Takeaway:

Industry stakeholders should closely track raw material inventories, policy changes (e.g., trade duties), and import-export movements for better pricing strategies and sourcing efficiency.

Also Read : Global Steel Industry Outlook: Moderate Growth Amidst Demand Gaps & Price Recovery SteelBazaar Monthly Recap – March 2025 Edition

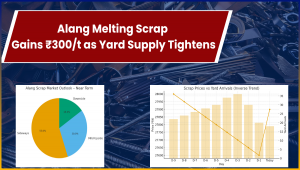

Alang Melting Scrap Up ₹300/t DoD Snapshot Melting scrap prices at Alang (ship-breaking yard, Guja...

Renewables 17-Nov-2025

India and France have made history by releasing a detailed “defence industrial roadmap,”...

Business 27-Jan-2024

India's recent unveiling of comprehensive guidelines for pilot projects heralds a major stride towar...

Energy 05-Feb-2024

In a groundbreaking move to fortify India's energy infrastructure, state-run oil companies have inje...

Large Corporate 20-Jan-2024

In recent years, the dynamics of the global steel industry have been significantly influenced by Chi...

Business 23-Feb-2024

Discover steel recycling trends across key countries like China, India, the USA, and Turkey in 2024....

Business 28-May-2025